Of IT Act Will Impact Non-ULIP Policies?")

With the brand new monetary 12 months across the nook, you will need to act now and make investments your cash right now to reap most returns.

The coverage that might escape the axe of this rule is – ULIPs or unit-linked insurance policy.

Tax incentives have at all times acted as a catalyst in making certain wider insurance coverage adoption. Though well-balanced and growth-oriented, probably the most awaited monetary occasion of the 12 months – Union Budget – turned out to be a wistful affair for these anticipating a tax rebate over and above the usual restrict on insurance coverage insurance policies. The proposal, as a substitute, acknowledged that insurance coverage insurance policies with over Rs 5 lakh annual premium bought after 01 April 2023 would not be eligible for tax exemption below Section 10 (10D).

The coverage that might escape the axe of this rule is – ULIPs or unit-linked insurance policy. ULIPs will proceed to observe the identical rule of LTCG (long-term capital good points) tax – if the yearly premium of a ULIP plan bought after 01 February 2021 exceeds Rs 2.5 lakh, then they are going to be topic to taxation, identical to each different equity-oriented funding.

While ULIPs reward buyers below beneficial market circumstances, additionally it is true that they bear a threat below unstable markets. So, how ought to one go about monetary planning in gentle of this latest announcement?

Now that the monetary 12 months involves an in depth, right here’s rounding up what this growth means and the way it impacts a median investor.

Union Budget 2023’s proposal concerning Section 10(10D)

In the Union Budget 2023, Finance Minister proposed that the maturity quantity for insurance coverage insurance policies with a cumulative annual premium exceeding Rs 5 lakh won’t be eligible for a tax rebate below Section 10 (10D). The announcement excludes ULIPs or unit-linked insurance policy and may have no tax implications on them. The rule is relevant for insurance policies purchased after 31 March 2023.

However, the proposal doesn’t impression the tax exemption relevant to the quantity obtained on the dying of the insured particular person. Since the higher restrict for taxation is Rs 5 lakh yearly, this received’t have an effect on most policyholders however it might impression HNIs (High Net-Worth Individuals) who normally would have insurance coverage premiums exceeding this restrict.

Last few days: Where do you have to make investments to reap most returns?

While conventional plans have come below the axe of taxation, there’s nonetheless time to make smart investments effectively earlier than the deadline and save up. Out of insurance-cum-investment choices, assured return plans are sometimes thought-about a viable avenue for each sort of investor since they don’t let your funds get affected by market volatility.

Your price of return is locked on the time of buy and the principal quantity in addition to returns are shielded from any fluctuations. The new-age assured return plans provide returns as excessive as 7.5% which might be utterly tax-free, relying on phrases and circumstances. They additionally include a life cowl that’s 10 instances the annual premium and in addition qualifies for tax advantages below Section 80C. This is why these plans are deemed to be an incredible different to different conventional choices like FD or PPF, and so on.

How the rule impacts your returns earlier than and after thirty first March?

With the brand new monetary 12 months across the nook, you will need to act now and make investments your cash right now to reap most returns. Let us illustrate how –

Let’s say you make investments Rs 1 lakh month-to-month within the plan for five years at a price of seven.5%. The complete maturity quantity will probably be Rs 1.03 crore together with the curiosity of Rs 43 lakhs. The tax legal responsibility is zero; this maturity quantity will probably be your take-home quantity.

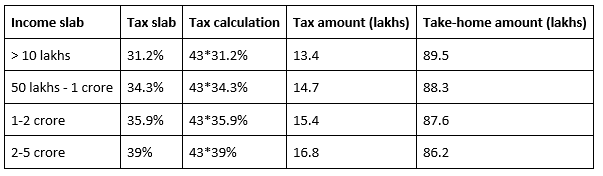

Here is what occurs if you happen to fall below the taxable bracket –

Now, if you happen to purchase a assured return plan earlier than 31 March 2023, your plan would by no means be counted within the taxable bracket even if you happen to cross the Rs 5 lakh restrict sooner or later. As against the above-mentioned vary of Rs 89 – 84 lakhs, your take-home quantity will probably be Rs 1.03 crore. So, select correctly and make investments early to take advantage of out of your financial savings and returns.

-The creator is president and CEO, Policybazaar.com.

Disclaimer:The views expressed on this article are these of the creator and don’t signify the stand of this publication.

Read all of the Latest Business News right here

{kind=link}