For consultant functions.

| Photo Credit: iStockphoto

The story to date: Recently varied Opposition-ruled States particularly from south India have claimed that they haven’t been receiving their justifiable share as per the current scheme of financial devolution. They have raised points about their lower than proportionate share of receipt in tax income when in comparison with their contribution in direction of tax assortment.

What is divisible pool of taxes?

Article 270 of the Constitution gives for the scheme of distribution of internet tax proceeds collected by the Union authorities between the Centre and the States. The taxes which might be shared between the Centre and the States embrace company tax, private earnings tax, Central GST, the Centre’s share of the Integrated Goods and Services Tax (IGST) and so forth. This division is predicated on the advice of the Finance Commission (FC) that’s constituted each 5 years as per the phrases of Article 280. Apart from the share of taxes, States are additionally offered grants-in-aid as per the advice of the FC. The divisible pool, nonetheless, doesn’t embrace cess and surcharge which might be levied by the Centre.

How is the Finance Commission constituted?

The FC is constituted each 5 years and is a physique that’s completely constituted by the Union Government. It consists of a boss and 4 different members who’re appointed by the President. The Finance Commission (Miscellaneous Provisions) Act, 1951, has specified the {qualifications} for chairman and different members of the fee. The Union authorities has notified the structure of the sixteenth Finance Commission beneath the chairmanship of Dr. Arvind Panagariya for making its suggestions for the interval of 2026-31.

What is the idea for allocation?

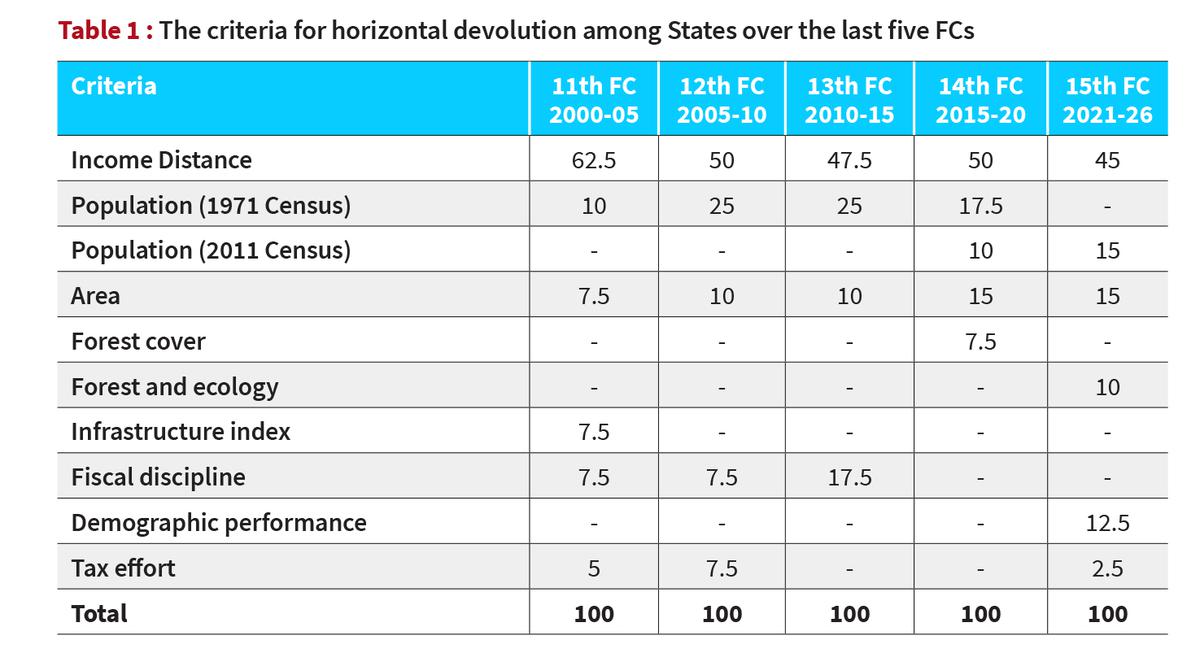

The share of States from the divisible pool (vertical devolution) stands at 41% as per the advice of the fifteenth FC. The distribution among the States (horizontal devolution) is predicated on varied standards. Table 1 lists the factors for horizontal devolution among the States from the eleventh to fifteenth FC.

The standards as per the fifteenth FC will be briefly defined as follows. ‘Income distance’ is the space of a State’s earnings from the State with highest per capita earnings which is Haryana. States with decrease per capita earnings could be given the next share to take care of fairness among States. ‘Population’ is the inhabitants as per the 2011 Census. Till the 14th FC, weightage was given for the inhabitants as per the 1971 Census however that has been discontinued within the fifteenth FC. ‘Forest and ecology’ take into account the share of dense forest of every State within the mixture dense forest of all of the States. ‘The demographic performance’ criterion has been launched to reward efforts made by States in controlling their inhabitants. States with a decrease fertility ratio can be scored increased on this criterion. ‘Tax effort’ as a criterion has been used to reward States with increased tax assortment effectivity.

What are the problems?

The Constitutional scheme has at all times favoured a robust centre in legislative, administrative and financial relations. However, federalism is a fundamental function and it’s important that States don’t really feel short-changed in terms of distribution of sources. While there are at all times political variations between the Union authorities and Opposition-ruled States that exacerbate the issue, there are real points that must be thought of.

Firstly, cess and surcharge collected by the Union authorities is estimated at round 23% of its gross tax receipts for 2024-25, which doesn’t type a part of the divisible pool and therefore not shared with the States. To present a perspective, the whole tax income for the 12 months 2022-23 (precise), 2023-24 (revised estimates) and 2024-25 (Budget estimates) of the Union authorities is ₹30.5, ₹34.4 and ₹38.8 lakh crore respectively. The State’s share was/is ₹9.5, ₹11.0 and ₹12.2 lakh crore respectively, which constitutes round 32% of the whole tax receipts of the Centre which is means lower than the 41% advisable by the fifteenth FC. Cess just like the GST compensation cess is for the reimbursement of loans taken to compensate States for the shortfall in tax assortment as a consequence of GST implementation for the interval 2017-22. Some of those quantities are additionally used for centrally sponsored schemes that profit the States. However, the States haven’t any management over these elements.

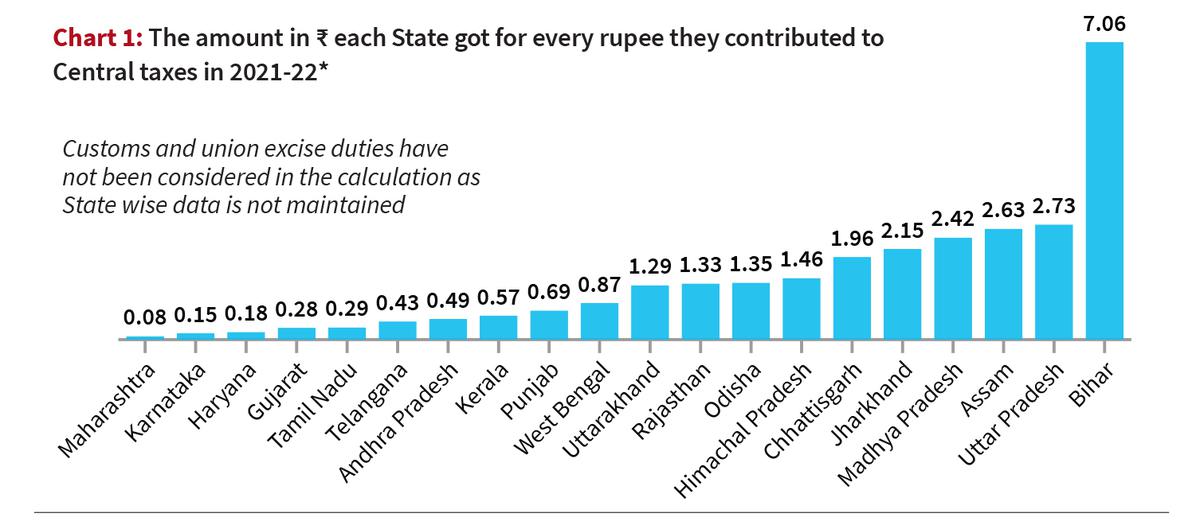

Secondly, the quantity every State will get again for each rupee they contribute to Central taxes reveals steep variation. Chart 1 depicts the identical for the 12 months 2021-22.

It will be seen that industrially developed States acquired a lot lower than a rupee for each rupee they contributed as in opposition to States like Uttar Pradesh and Bihar. This is partly as a consequence of the truth that many firms are headquartered in these State capitals the place they might remit their direct taxes. However, this variation can be attributed to the distinction in GST assortment among varied States.

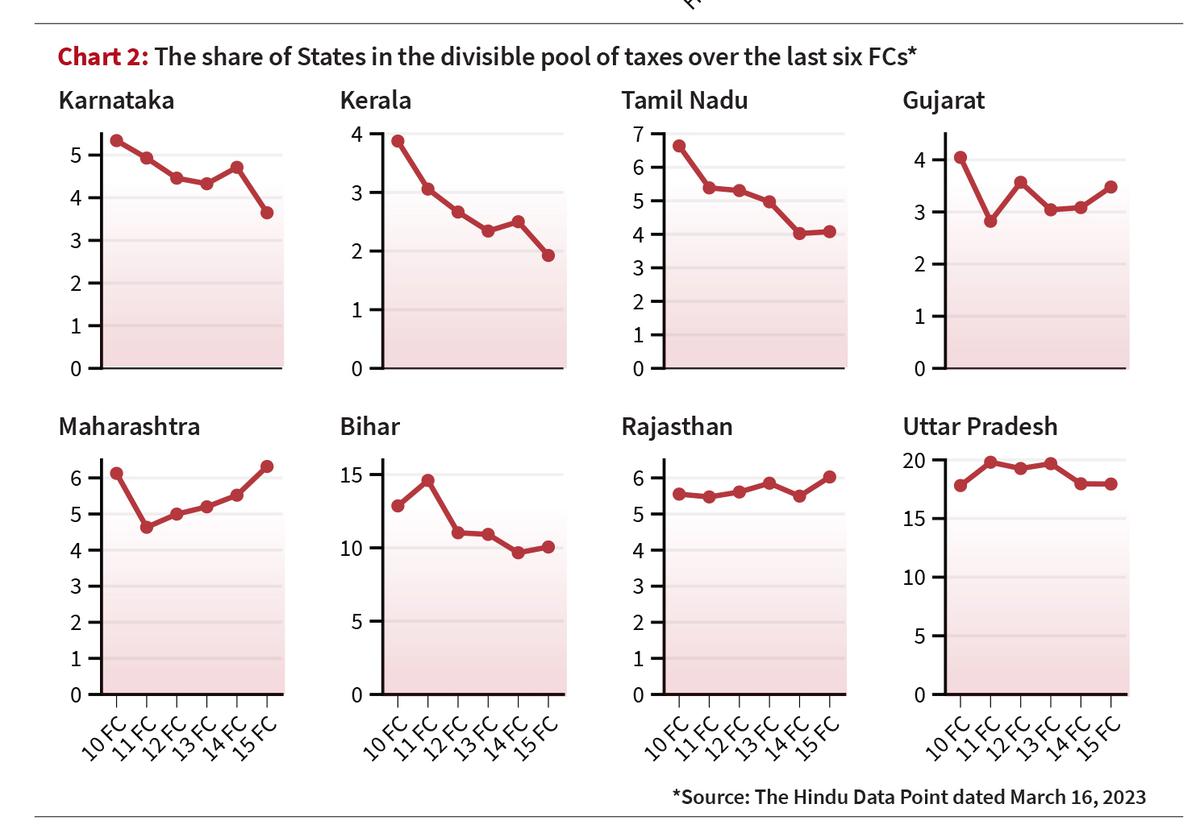

Third, the proportion share within the divisible pool of taxes has been decreasing for southern States over the past six FCs as will be seen in Chart 2.

This is attributable to the upper weightage being given for fairness (earnings hole) and desires (inhabitants, space and forest) than effectivity (demographic efficiency and tax effort). Finally, grants-in-aid as per the advice of the FC varies among varied States. As per the fifteenth FC, there are income deficit, sector-specific and State-specific grants given to numerous States in addition to grants to native our bodies which might be given based mostly on inhabitants and space of States.

What will be the way in which ahead?

It should be famous that States generate round 40% of the income and bear round 60% of the expenditure. The FC and its suggestions are supposed to assess this imbalance and suggest a good sharing mechanism. It is the duty of all States to contribute in direction of the extra equitable improvement of our nation. However, there are three vital reforms which may be thought of for sustaining the stability between fairness and federalism whereas sharing income.

Firstly, the divisible pool will be enlarged by together with some portion of cess and surcharge in it. The Centre must also regularly discontinue varied cesses and surcharges it imposes by suitably rationalising the tax slabs. Secondly, the weightage for effectivity standards in horizontal devolution ought to be elevated. GST being a consumption-based vacation spot tax that’s equally divided between the Union and the State signifies that State GST accrual (inclusive of Integrated GST settlement on inter-state gross sales) ought to be the identical because the Central GST accrual from a State. Hence, relative GST contribution from States will be included as a criterion by offering appropriate weightage in future FCs. Finally, much like the GST council, a extra formal association for the participation of States within the structure and the working of the FC ought to be thought of.

These are measures that must be applied by the Centre after dialogue with all of the States. It can be crucial that the States uphold ideas of fiscal federalism by devolving enough sources to native our bodies for vibrant and accountable improvement.

Rangarajan. R is a former IAS officer and writer of ‘Polity Simplified’. He presently trains civil-service aspirants at ‘Officers IAS Academy’. Views expressed are private.

{kind=link}